From Fawry to Feloosy, FinTech is finally gaining a foothold

As Egypt’s start-up scene continues to draw attention from global media, expect to hear more about FinTech. Short for financial technology, FinTech firms seek to develop new technologies that creatively streamline financial transactions.

The FinTech field has exploded over the past three years. According to The Economist, equity investment in FinTech companies tripled from US$4 billion in 2013 to more than $12 billion in 2014. However, of that $12 billion, less than a quarter went to non-Silicon Valley firms.

This may be changing. While lower-profile than their Silicon Valley counterparts, a number of Egyptian start-ups have been successful in the financial technology sector — offering services that have changed the way many Egyptians spend and save. Investors are beginning to take note.

Earlier this year, Dubai-based payment platform Payfort announced the launch of an accelerator to provide $400,000 in funding and expertise to FinTech firms. Weeks before that, payment-facilitator Dopay raised $2.4 million in funding to expand its services in Egypt and Ghana. These announcements come months after Egypt’s most noticeable FinTech success. In November, Egyptian electronic payment firm Fawry was purchased for $100 million, the largest ever exit for a FinTech firm in Egypt.

In the coming years, FinTech firms are expected to become increasingly central to lives and businesses across the Middle East, boosting the region’s startup environment by expanding access to funding and markets. The stories of Fawry and Feloosy — two of Egypt’s existing FinTech firms —highlights the opportunities and challenges Egypt presents for this growing sector.

Fawry

Fawry is a name that most Egyptians are familiar with — the company is the market leader in electronic bill payment in Egypt, with outlets sporting its blue and yellow logo seemingly everywhere. The service allows Egyptians to pay almost all of their bills in one place, securely and conveniently, either online or via physical service points. Fawry’s purchase in November represents a major Egyptian FinTech success story, one which has paved the way for other startups.

Fawry was founded in 2009 by Ashraf Sabry, a civil engineer by training, who has spent most of his career in information technology. In his time with IBM and Raya Corporation, Sabry says he recognized the need for a better system of bill payment, and saw potential for a long-term business. “IT is a project based business. The nature of the business is sporadic,” he explains. “A business that had a continuous stream of revenue was interesting.”

At the time, the market for electronic bill payment was wide open. “There were a number of initiatives, but there was nothing really material,” Sabry says. “We were the first to enter the market.” The company started with telecom bill payment and soon moved into utilities, ticketing and education, allowing customers to pay their bills at banks and other outlets rather than the office where the bill was due. For each transaction, Fawry collects a fee.

Fawry’s value comes from its network as much as it does from its technology. As the first-mover, the company was in a position to rapidly expand the number of outlets and methods of payment to online and mobile. Six years after it was founded, Fawry now offers more than 60 types of bill payment services at 50,000 service points, ranging from corner kiosks to ATMs. Transactions have increased from 1,000 per day at the end of 2009 to currently more than 1.3 million transactions per day. The company now holds around 85 percent of the Egyptian bill paying market, Sabry says.

Feloosy

Three months before the Fawry purchase announcement, in August 2015, Karim Beltaji and his team created a Facebook page with a message: “Coming Soon: The new way to effectively manage your money online.” Compared to Fawry, Feloosy is still in its infancy. The company is in its pilot stage, its website operational but not yet accepting deposits.

Karim Beltaji, CEO of Feloosy, is a serial entrepreneur. Leaving his job as an investment banker with Citi Group in 2013, he moved to Berlin to learn more about the German startup scene. After working with a couple of startups and incubators, he returned to Egypt in 2014 to work on FinTech concepts for the Egyptian market.

The concept he developed is similar to existing models in other markets, but is tailored to Egypt. Feloosy’s goal is to make saving and investing easier for young Egyptians by offering a platform to deposit small amounts of money, which then are invested by the company’s financial partners in low and medium risk instruments like Money Market Funds and Exchange-Traded Funds. Depositors can then keep track of how their money is growing. Feloosy takes a percentage of profits, but does not charge transaction fees. The company’s interests are aligned with its investors: “Any money we make is directly linked to the growth of your wealth and you achieving your goal,” its website explains.

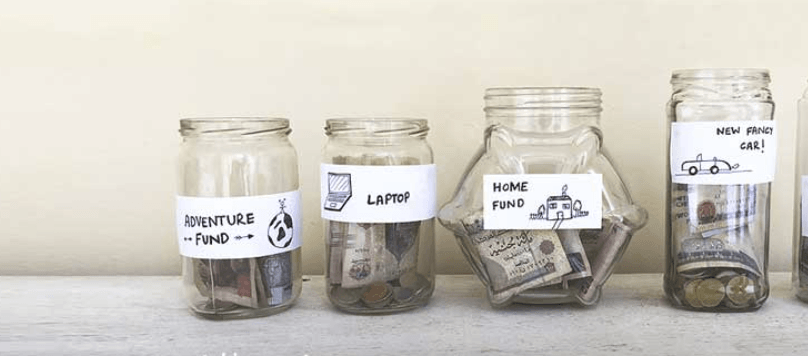

“Because financial literacy is quite low in Egypt, investing can be quite intimidating to people,” Beltaji says. To counter this, Feloosy built a feature into the site that lets users see their savings in terms of goals they set for themselves — be it a new laptop, a car or a vacation. By translating savings into tangible items, Feloosy hopes to help users better understand their savings and goals.

Changing challenges

While Fawry and Feloosy are at different stages of development, they face many of the same challenges.

Among the largest, Fawry’s Sabry says, is building trust and awareness in a market that is unfamiliar with financial tech. Or, as he puts it, “Convincing people that Fawry is correlating with good things because people know they can pay all their bills there.” Sabry says FinTech firms must build trust through a clear image for the company and a technology that works well.

Feloosy shares this challenge. Egypt has a massive unbanked population and trust in financial schemes is generally low, Beltaji recognizes. In Egypt and abroad, he says that “banks have been very bad at aligning their interests with their customers interests,” something Feloosy has sought to overcome. The Feloosy website carefully explains its process and how the company makes money as customers do — a transparency Beltaji feels Feloosy needs to be successful.

Beltaji also notes that most young Egyptians save very little and, until an age much later than much of the rest of the world, rely on family and friends for financial security. Promoting financial independence among Egyptians is both a major challenge and goal for Feloosy, he says.

Feloosy must also contend with the level of financial and online penetration in Egypt. Beltaji says that figures which put online penetration in Egypt between 40 and 50 percent are likely inflated or misleading, noting that those figures better represent Facebook penetration than Egyptians’ use of the web. Further, even those who shop online rely on cash on delivery and online financial transactions remain rare.

Another major challenge both companies have faced is funding. When starting Fawry, Sabry says it was difficult to find investors. “We had to convince people to put money in,” he recalls.

While finding investment was a struggle for Fawry in 2009, interest in the field seems to be growing. When Feloosy began its seed round late last year, Beltaji said the response was positive. However, although there may now be more money available for FinTech than in years past, not all investors are good fits. “Unfortunately, many local investors seem to be impatient or even unwilling to back a business with a long term view and target more short term profitability over long term growth,” he says.

Opportunities

Both CEOs agreed that Egypt is unique in the size of its opportunities for FinTech and that much of the groundwork has now been laid — in large part due to Fawry. Beltaji says: “I really admire what Fawry has achieved and what they do. Egypt isn’t an easy environment … People are more comfortable managing their money in an electronic way because of Fawry.”

Beltaji says that FinTech startups in Egypt are in the “leapfrog” business, seeking to encourage Egyptians to skip traditional avenues altogether in favor of electronic financial services: “Because only 10 to 13 percent of people are banked, we can immediately digitize people. The opportunity is huge.” This is an major area where Egypt’s challenges become opportunities for startups.

Around the world, FinTech companies generally have a mutually-beneficial relationship with existing institutions, helping consumers participate in mainstream financial systems. This is the case for Fawry, which helped businesses collect payments and the government collect revenues. It is also the plan for Feloosy, which will make it easier for Egyptians to invest in Egypt’s financial system.

But while Fawry has proven its value to government and private institutions, much more must be done to help Egyptian FinTech startups take hold and work with the institutions in place, especially as a number of challenging regulations remain. "Legally, there are questions that really have to be figured out,” says Salma al-Hariry, managing director of government-backed technology hub EgyptInnovate. "New FinTech startups moving into the market need to build a symbiotic relationship with the government and institutions in place,” she says. “Working through the banking system, using what is already there and building partnerships is the fastest way to grow new technologies and innovations." Building the bridges between startups and other crucial stakeholders is the next step for Egyptian FinTech firms.

تقارير ذات صلة

Co-working spaces spread, but lack resources

The walls of Al-Maqarr, a co-working space in Cairo’s eastern neighborhood of Heliopolis, are lined with images of its projects. "During college, we used to hold our meetings in cafes…

Egypt rises to 112 in Doing Business rankings, but officials still displeased

Egypt rose one place to rank 112 out of 189 economies surveyed for the World Bank’s annual Doing Business 2015 report, which measures the ease or difficulty with which entrepreneurs…

Nuggets of advice for entrepreneurs from RiseUp 2014

It's rare to have the likes of Dave McClure, Fadi Ghandour, Chris Schroeder, Hala Fadel, Ahmed al-Alfy and Wael Fakharany in the same space at the same time. It's even…

Your support is the only way to ensure independent, progressive journalism survives.

You have a right to access accurate information, be stimulated by innovative and nuanced reporting, and be moved by compelling storytelling. Subscribe now to become part of the growing community of members who help us maintain our editorial independence.

Join us