Explainer: Too much steel? What are the market conditions behind the decision to liquidate Egyptian Iron and Steel

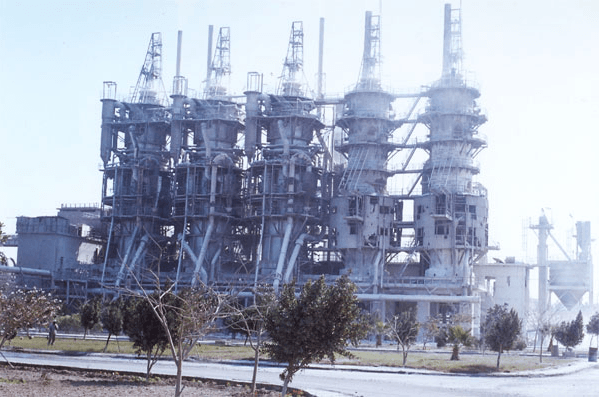

“The common factor between the Egyptian Iron and Steel Company and all other steel companies in Egypt is the dysfunctional production capacity,” says a former manager at the Egyptian Iron and Steel Company, which is getting ready to exit the Egyptian market 67 years after its foundation based on the liquidation decision passed just over a month ago.

The source, who spoke to Mada Masr on condition of anonymity, pointed to the marked difference between the actual production of iron and steel companies in Egypt and their production capacity, or in other words, the difference between what companies actually produce and what they could have produced if they operated on full capacity.

In FY 2019/2020, the Egyptian Iron and Steel Company produced 107,662 tons, whereas the company’s annual production capacity stands at 1.2 million tons, which means that actual production barely exceeded 10 percent of the company’s production capacity — a consequence of the continuous malfunctioning of some furnaces and the total breakdown of much older furnaces.

“Generally speaking, the iron and steel industry does not exceed 60 percent of its production capacity due to the low levels of local demand,” says Mohamed Hanafy, Head of the Metallurgical Industries Chamber in the Federation of Egyptian Industries, adding that any development plan pushed forward by the critics of the liquidation decision will not be capable of driving the company’s production up to meet its capacity. He also reiterated that the iron and steel industry as a whole does not meet its production capacity due to the saturation of the local market.

At first sight, the saturation of the market might explain why one or two companies might exit the market, a point of view that is propounded by those who support the decision to liquidate the Egyptian Iron and Steel Company. However, that very same saturated market imports quadruple the amount it exports.

How can we explain the discrepancy between this “hunger” for imports and the “glut” of production?

According to international trade estimates, semi-finished casting products — mainly billets — make up the largest portion of Egypt’s steel imports. According to Trade Map, Egypt’s imports of semi-finished casting products in 2019 cost more than US1$ billion, which is about a third of Egypt’s total iron and steel imports and more than 40 percent of Egypt’s total iron and steel exports.

This is the core of the iron and steel crisis in Egypt because the industry needs large amounts of semi-finished casting products to produce finished goods for the local market.

The structure of the iron and steel industry in Egypt explains this huge burden of semi-finished casting products imports. The industry consists of four vertically integrated companies out of a total of 34 companies that operate in the industry: the Egyptian Iron and Steel Company, the Suez Steel Company, the Ezz Dekheila Steel company, and Beshay Steel.

The vertically integrated companies produce iron from extracted raw materials up to the finished product, which means they pass through all levels of production. The Egyptian Iron and Steel Company is among those.

As for semi-integrated companies, they begin production midway through the process. In other words, they do not rely on mining for raw materials but on iron scrap, which is recycled so that it can be used to produce finished goods. This happens via the iron billet production process. The Egyptian market has eight semi-integrated companies. The iron and steel industry in Egypt as a whole started in the 1940s as a semi-integrated industry, whereby companies like Delta Steel, El Ahleya for Iron Trade and Egyptian Copper Works used iron scrap for production.

The vast majority of iron and steel companies in Egypt are rolling mills, which means that they purchase billets and reshape them, mostly to produce rebar. Rolling converts semi-finished casting products into finished products. This means that the remaining 22 companies that make up the majority of Egypt’s steel industry work on the last level of the production process.

Because of the proliferation of companies that work on this one level of the production process, the billet imports continue to increase. “The other integrated companies produce billets but do not offer them for sale on the market, except very rarely, because they use them in their own production process,” says the former manager in the Egyptian Iron and Steel Company. This means that as local production increases, regardless of whether it sells in the local or foreign markets, imports of billets will continue to increase as well.

As an exception, however, Egyptian Iron and Steel is allowed to sell billets to local producers. “Until now, the Egyptian Iron and Steel Company is the main local source of billet production that rolling mills rely on,” the former manager says. “Many of the previous development plans focused on temporarily halting the production of finished goods and accelerating the production of billets because the latter is capable of generating huge profits for the company since rolling mills are always in urgent need for billets.”

Given that the Egyptian Iron and Steel Company is the only local source for billets, it subsequently cannot be part of the “production glut” crisis. “The ‘glut’ is essentially concentrated in rebar production, which the Egyptian Iron and Steel Company does not do,” the former manager says. “The company has one small unit for rebar production that has not operated in about 10 years.”

The production glut in the iron and steel industry, especially in rebar production, was preceded by a period of scarcity almost 30 years ago.

According to the Metallurgical Industries Chamber, the iron and steel sector was marked by steady growth at the beginning of the 1990s, which was commensurate with economic changes, development plans and the increase in infrastructure construction in all facilities that depended on rebar at the time. During the 1980s and early 1990s, Egypt imported about 1.5 million tons per year. Therefore, many investors were encouraged to enter the iron and steel industry, starting with rolling projects using imported steel bars. They then expanded to add smelting units, companies that produce billets, and rolling mills to sell in the local market and for export.

At the same time, as the private sector was increasingly contributing to the GDP and labor market following a loan agreement with the International Monetary Fund, it also entered the steel industry. During this period in the early 1990s, private companies were provided with substantial support, such as tax exemptions, investment incentives, allocation of lands at low prices and generous subsidies in the energy sector, according to what Amr Adly, an assistant professor of economics at the American University in Cairo, stated in a 2017 report published by Carnegie Middle East Center.

“In the last 30 years, we witnessed a huge push of investments into the iron and steel sector, which is what led us to the situation we have now: an obvious slump, especially with regards to rebar, which forces companies to sometimes sell at cost,” says the former manager at the Egyptian Iron and Steel Company.

Despite this slump, in 2016 the National Service Projects Authority of the Armed Forces bought 40 percent of the Suez Steel shares, one of the four vertically integrated companies in Egypt, paid off more than LE5 billion in debt owed to the banks, and increased the company’s capital to LE13.9 billion, which included LE2 billion in new investments. All of this allowed the authority to secure an 82 percent share in the company.

An internal research memo written by the Oxford Economics-owned NKC African Economics firm, a copy of which Mada Masr obtained, states that the projects authority raised the productivity of Suez Steel after it acquired the company, which exacerbated the production surplus crisis even more.

“In any case, the military does not obey the market dynamics that other players are subject to, as is evident by the available indicators, such as the cost of energy and transportation and other factors. This suggests that the military is not facing any pressures on its profitability, which other players in the market are facing [due to the production glut],” states an economic analyst at the Egyptian Center for Economic Studies, who spoke to Mada Masr on condition of anonymity. In the analyst’s view, this explains why the military would enter a market that is already experiencing a production glut, which threatens the profitability of other companies.

During a webinar hosted by the Egyptian Center for Economic Studies, Public Enterprise Minister Hisham Tawfik did not respond to Mada Masr’s question about how the Armed Forces continues to thrive in the market without struggles despite the production glut, while this glut justifies the exit of the Egyptian Iron and Steel Company from the market. However, the analyst from the center who spoke to Mada Masr stated that the Egyptian Iron and Steel Company does not enjoy the same privilege of noncompliance to market dynamics that the Armed Forces has, and the public enterprise minister believes that the latter must completely comply with the terms of the market.

In light of the saturation of the local market with Egyptian steel products, exports became the main channel to absorb the production capacity of the iron and steel sector, especially after the devaluation of the Egyptian pound in 2016. It was expected that the export sector would see a boost due to the lower price of Egyptian products in international markets. However, the available estimates show that the rate of exports has remained relatively constant after the devaluation of the pound. And while 2018 saw a relative increase in exports, they subsided again in 2019.

Egyptian Iron and Steel Association Chief Executive Alya al-Mahdy believes that Egyptian iron and steel exports face many competitive challenges on the international market, the most important of which is the high cost of energy.

“The cost of supplying electricity to iron and steel factories is the highest in comparison to other steel-producing countries. The cost of 1 kilowatt-hour in Egypt is about 6 euro cents, whereas 1 kilowatt-hour in the European Union cost 2.4 euro cents in mid-2020. The industry in Egypt pays $4.50 per 1 million British thermal units, which is more than double the price of its supply to the industry in Europe and the United States, which pays $1.40 and $1.80 per million British thermal units respectively,” states the official webpage of the Egyptian Iron and Steel Association.

Mahdy pointed out that the decline in global economic growth is also a challenge to Egyptian steel exports since there is an overall global drop in demand.

تقارير ذات صلة

Worker-management rift remains as state pharma company reopens after strike

One trade union representative called the move to shutter the firm amid the strike 'unprecedented'

The Kafr al-Dawar textile company: On the road to liquidation

Kafr al-Dawar reflects the state’s desire to back out of the sector, analysts say

Public sector giant Egyptian Iron and Steel Company to be liquidated despite opposition

Monday's decision has already faced substantial pushback.

Your support is the only way to ensure independent, progressive journalism survives.

You have a right to access accurate information, be stimulated by innovative and nuanced reporting, and be moved by compelling storytelling. Subscribe now to become part of the growing community of members who help us maintain our editorial independence.

Join us